If you are like many commercial auto insurance buyers, you probably really pay attention to those costs once a year when you shop for coverage. But you really should pay closer attention all year long because cost inflation in commercial auto coverage has been happening for over a decade, and small fleets feel the impact disproportionately to large fleets. Why do your insurance costs continue to rise?

The answer is really just basic economics. The demand for coverage has exceeded the supply of premiums used to pay claims going all the way back to 2011. Simply put, the number and cost of insurance claims has exceeded the amount of premium paid into the pool to pay losses. There are many reasons for this: increasing crash frequency; increased cost to repair damages; inflated medical costs; the impact of “nuclear verdicts”; litigation financing and a host of other “social factors” have yielded greater insurance losses and underwriters have not collected enough premium to cover the costs. The response of the insurance industry has been to increase rates. Commercial auto rates have increased quarterly for the past 40 quarters but increasing rates has not solved the financial problem.

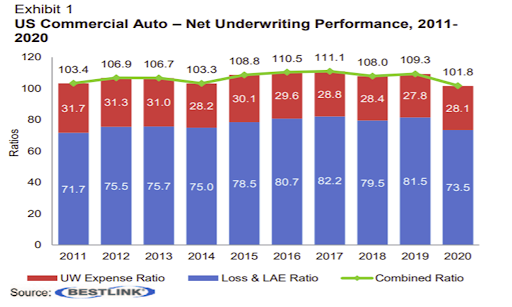

Insurance companies use a ratio to measure profitability. Costs are put into two buckets: losses (including defense and adjusting costs) and expenses. The two buckets of cost combined are referred to as the “Combined Ratio”. A Combined Ratio above 100 means that underwriters are not collecting enough premium to cover the costs. Insurance companies want to avoid underwriting losses. As you can see from the chart below, the Commercial Auto market has experienced underwriting losses every year going back to 2011.

So, premiums continue to go up. In theory, eventually - as rates rise - more insurance capacity enters the marketplace which in turn tends to bring down rates. Insurance companies do not rely solely on underwriting profitably to make money. In addition to underwriting profits, insurance companies generate investment income with their portfolio of earned premium. But in low interest rate environments like we have experienced for the past 20 years, insurance companies place a greater importance on underwriting results. Even additional capacity in the marketplace has not resulted in lower premiums, as underwriters try to bring premium in line with costs. The reason is that costs continue to rise at a greater rate than additional premium/underwriting capacity.

Carriers feel this impact when they apply for insurance coverage. Until losses are less than the amount of premium collected, you can expect your rates to continue to increase. While you can’t really increase the underwriting capacity, you can be part of the solution – and not by paying more premium into the pool!

How? Well, it is a very simple formula – reduce the number and severity of losses. Become the kind of risk the underwriters want to insure – you know, the one who pays premium and doesn’t have losses. Because if you are the other type of risk, the one who pays premiums AND generates excessive losses, you might find yourself paying rates you can’t afford, if you can find someone who will insure you at all.

So, the answer is quite simple – be safe. Invest in improving your safety results. Start by not referring to accidents as “accidents”. Refer to events as “crashes”, and presume that you can prevent most, if not all of them – even the crashes caused by the mistakes of other motorists. Fleet owners really must start with that mindset. Crashes need to be as unacceptable to you as not having a load to haul with your available tractor and trailer. In fact, as a fleet owner your mindset should be that you would rather park the rig than allow it to be operated unsafely.

Most people certainly are responsible and don’t want to have crashes – obviously you don’t want to have your rig wrecked in a crash and you certainly do not want to see people get hurt. You don’t expect that to happen to you. But wishing and hoping are not strategies. So, if you are really committed to lowering your risk profile and, by extension, your costs and thus making your business more profitable, what do you do?

Implement an effective safety plan and follow it in a disciplined way. Don’t trust to luck. What does an effective safety program look like? Well, there are certain principles or elements that decrease the likelihood of crashes within your fleet. And, if you are operating your own rig, there are safe driving practices you yourself can follow that will reduce risk. You will find these elements in the Model Safety Plan ICSA will soon introduce, along with First Gear, a proven online driver training tool that will soon be made available to ICSA members at no cost. Here are key components of a safe operation:

- Hire conscientious, capable and competent drivers. No matter how urgently you are looking to hire a driver for that rig you are paying for, never compromise your expectations just to fill a seat. Implement meaningful hiring standards; conduct an effective background check to ensure the individual meets your expectations; ensure the individual is drug free, properly prepared, a competent operator, and physically able to do your job safely. Properly orient every new driver to ensure they are truly prepared before sending them out on that first load.

- Set simple clear safety expectations that everyone agrees to and that are sensible. Be particularly attentive to imposing clear expectations around four key driving behaviors: speed, following distance (managing the space around the vehicle), distraction and fatigue. One or more of these issues generally factors into a crash. Your expectations must set clear standards around each of these factors.

- Observe driving performance and provide feedback. If you have not already done so, install forward facing event-recorders in your truck cabs. Ensure your driver and a responsible manager are seeing the events and data gathered that quantify the driver’s performance relative to your expectations. Provide timely and specific feedback and create accountability for the driver to adjust their driving practices to conform to the expectations they have already agreed are reasonable. Our ICSA team is ready to help you expedite the installation of event recorders to help your business.

- Report crashes immediately to your insurance company, preferably from the scene of the crash. Why? Timely reporting reduces the cost of crashes. If you delay reporting for any reason, the cost of that claim is going to end up being much higher. Don’t make the mistake of delaying reporting. A delay may also cause your insurance company to non-renew your coverage at the end of your policy term.

- Implement and follow a zero-tolerance drug and alcohol policy. As a platinum ICSA member, you have already implemented hair testing, which is eight times more likely to catch that habitual user, and you have also used ICSA’s sample zero-tolerance policy to implement your own policy.

- Provide regular training to your drivers. Defensive Driving training is particularly helpful to teach and reinforce driving behaviors and techniques that help the driver prevent crashes caused by the mistakes of others.

- Recognize and reward good safety performance. Make it meaningful for the driver. Sincere, timely expressions of gratitude are impactful. Compensate your driver for their valuable work and connect that compensation to their safety performance and results.

- Hold everyone in your business to the standards you have set and create individual ownership for safety. Establish key metrics to measure your performance and outcomes. Examples might include using the Smartdrive safety score or equivalent; recordable DOT crash rates per million miles; injury rates, et cetera. Create ownership for results in these key areas. As the fleet owner these should be some of your most important business metrics.

All these actions will cultivate a culture of safety. As more and more fleets get into this cadence of safety performance, the industry’s safety culture will improve, crashes will be reduced and insurance costs will follow. There is no shortcut to lower insurance costs – safety is the key!

Thank you for joining ICSA and taking this big step toward improving highway safety. Be on the lookout on our website for more tools and information to help you implement your own, effective safety program.